Advantages and Disadvantages of Cost Accounting:

Cost accounting serves as a fundamental tool for businesses, offering a systematic approach to financial management and decision-making. It provides invaluable insights into the intricacies of production costs, aiding in price fixation, performance evaluation, and strategic planning. However, like any system, cost accounting is not without its drawbacks. Understanding the advantages and disadvantages is crucial for businesses seeking to harness its benefits while navigating its limitations. In this article, we will explore the advantages and disadvantages of cost accounting.

Advantages of Cost Accounting:

Cost accounting plays a crucial role in the efficient management of a business, offering various advantages that contribute to its overall success. Here are some key advantages of cost accounting:

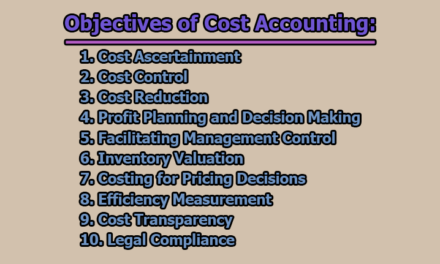

1. Helpful in price fixation: Cost accounting provides a detailed breakdown of costs associated with production, allowing businesses to set appropriate and competitive prices for their products or services. This ensures that prices cover costs while remaining attractive to customers.

2. Detect profitable as well as unprofitable business activities: By analyzing costs associated with different business activities, cost accounting helps identify both profitable and unprofitable ventures. This insight enables businesses to allocate resources more efficiently, focusing on activities that contribute positively to the bottom line.

3. Guide in price reduction: Cost accounting helps identify areas where costs can be reduced without compromising product or service quality. This guidance is invaluable in making informed decisions to streamline operations and enhance overall cost-efficiency.

4. Adaptable in nature: Cost accounting can be customized to suit the specific needs of different industries and businesses. Whether it’s job costing, process costing, or activity-based costing, the flexibility of cost accounting systems allows for adaptation to various organizational structures and industries.

5. Assist in proper planning and decision-making: Cost accounting provides vital information for business planning and decision-making. Managers can use cost data to create realistic budgets, set achievable goals, and make informed decisions about resource allocation, expansion, or diversification.

6. Assist in controlling expenditure: Cost accounting facilitates the monitoring and control of expenditures. By tracking costs at various stages of production or service delivery, businesses can implement effective cost control measures to prevent unnecessary expenses and improve overall financial performance.

7. Facilitate performance evaluation: With cost accounting, businesses can evaluate the performance of different departments, products, or services. This evaluation helps in identifying areas of improvement, rewarding efficient units, and addressing issues that may hinder overall organizational performance.

8. Enhance transparency and accountability: Cost accounting promotes transparency in financial reporting by providing a detailed breakdown of costs. This transparency fosters accountability within the organization, as managers can be held responsible for the costs associated with their respective areas of operation.

9. Improve inventory management: By tracking the costs of raw materials, work-in-progress, and finished goods, cost accounting helps optimize inventory levels. This, in turn, minimizes holding costs, reduces the risk of stockouts, and ensures a smooth production process.

10. Facilitate compliance with regulations: Cost accounting helps businesses comply with regulatory requirements by providing accurate and detailed financial information. This is particularly important for industries with specific cost reporting standards or those subject to government regulations.

Disadvantages of Cost Accounting:

While cost accounting offers valuable insights and benefits to businesses, it is essential to recognize its limitations and potential disadvantages. Here are some key disadvantages of cost accounting:

1. Complexity and Implementation Costs: Implementing a comprehensive cost accounting system can be complex and costly. Small businesses, in particular, may find it challenging to allocate resources for the installation and maintenance of sophisticated cost accounting systems.

2. Subjectivity in Cost Allocation: Cost allocation involves assigning indirect costs to various products or services. The process can be subjective and may rely on estimates, leading to potential inaccuracies. This subjectivity can impact the reliability of cost data and subsequent managerial decisions.

3. Overemphasis on Historical Data: Cost accounting relies heavily on historical data, which may not accurately reflect future conditions. Economic changes, technological advancements, or shifts in market dynamics can render historical cost data less relevant for decision-making.

4. Inflexibility: Some cost accounting systems may lack flexibility, making it challenging to adapt to changes in the business environment or alterations in production methods. This inflexibility can limit the system’s ability to provide timely and relevant information.

5. May Lead to Short-Term Focus: Cost accounting often emphasizes short-term cost reduction, potentially at the expense of long-term strategic goals. Focusing solely on immediate cost-cutting measures may hinder investments in innovation, quality improvement, or employee development.

6. Not Suitable for Every Industry: Certain industries, such as service-oriented businesses, may find traditional cost accounting methods less applicable. Intangible factors like customer satisfaction and employee performance can be challenging to quantify accurately in a cost accounting framework.

7. Dependence on Assumptions: Cost accounting relies on various assumptions, such as the relationship between variable and fixed costs. Changes in these assumptions, which may occur due to shifts in production volume or market conditions, can impact the accuracy of cost estimates.

8. May Encourage Suboptimal Decision-Making: Managers relying solely on cost accounting information may make decisions solely based on minimizing costs without considering broader strategic implications. This approach could lead to suboptimal choices, such as sacrificing product quality or customer satisfaction.

9. Risk of Overhead Allocation Issues: Allocating overhead costs to products or services can be challenging, leading to potential distortions in cost data. If overhead costs are not allocated accurately, it may result in incorrect pricing decisions or misguided efforts to reduce costs.

10. Time-Consuming: The process of collecting, analyzing, and interpreting cost data can be time-consuming. This time requirement may delay the availability of crucial information for decision-making, particularly in fast-paced and dynamic business environments.

11. Resistance from Employees: Employees may resist cost accounting initiatives, especially if they perceive it as a tool for evaluating their performance. This resistance can hinder the successful implementation of cost accounting systems and limit their effectiveness.

In conclusion, cost accounting stands as a double-edged sword in the realm of financial management. Its advantages, including aiding in price fixation, facilitating decision-making, and enhancing transparency, underscore its significance in the business landscape. However, businesses must navigate the potential pitfalls, such as the complexity of implementation, subjectivity in cost allocation, and the risk of short-term focus. Striking a balance, businesses can optimize the benefits of cost accounting while mitigating its limitations. In doing so, they empower themselves to make informed decisions, streamline operations, and adapt to the ever-evolving dynamics of the market, ensuring a comprehensive and strategic approach to financial management.

is an experienced educator and academic currently serving as a Lecturer at Nurul Amin Degree College. With a career dedicated to student development and institutional excellence, he brings a wealth of classroom expertise and pedagogical knowledge to his current role. Before joining the faculty at Nurul Amin Degree College, he served as an Assistant Teacher at Zinzira PM Pilot School and College.

{kind=link}